- About Us

- Our Services

- Perspectives

- …

- About Us

- Our Services

- Perspectives

- About Us

- Our Services

- Perspectives

- …

- About Us

- Our Services

- Perspectives

Turnaround Strategy (Part 1 of 2):

How to recover from financial distress

1. Overview

During the Covid-19 crisis, while some companies have found good opportunities, many suffered financial distress, and are possibly at risk of becoming insolvent. Even in the best of times, we are increasingly entering a world of constant disruption, which could force companies that have performed well in the past to fall into financial difficulties.

The objective of this 2-part Thought Leadership is to equip business owners like yourselves with additional tools (beyond government grants and loans) that you could quickly use and implement to get your companies into a better state.

Part 1 focuses on helping you gain a better understanding of your company’s cash flow situation.

In Part 2, we will discuss how you could extend your company’s cash runway, and subsequently develop strategies to help you bring your companies back to breakeven or profitability.

2. Understanding your cash flow situation

Before developing any strategies to turn around your business, it is important to have an in-depth understanding of your company’s current financial situation.

This could be achieved in 3 steps:

Step 1: Switch to Cash Accounting

To diagnose financial distress, choose Cash Accounting over Financial Accounting.

Financial Accounting assumes that your business will continue operating indefinitely until proven otherwise (‘going concern’), which might not be suitable for a distressed company, since a distressed company is at risk of being forced out of business. Under Financial Accounting, revenue and expenses are recognised when earned and incurred respectively, regardless of whether cash is received or paid. This could give you a false sense of security.

Cash Accounting, on the other hand, gives you a better sense of reality as it tracks the actual cash flow in and out of your business. This is important because cash is the lifeline of all companies. Your company’s survival is dependent on whether you have sufficient cash to meet your obligations and financial liabilities.

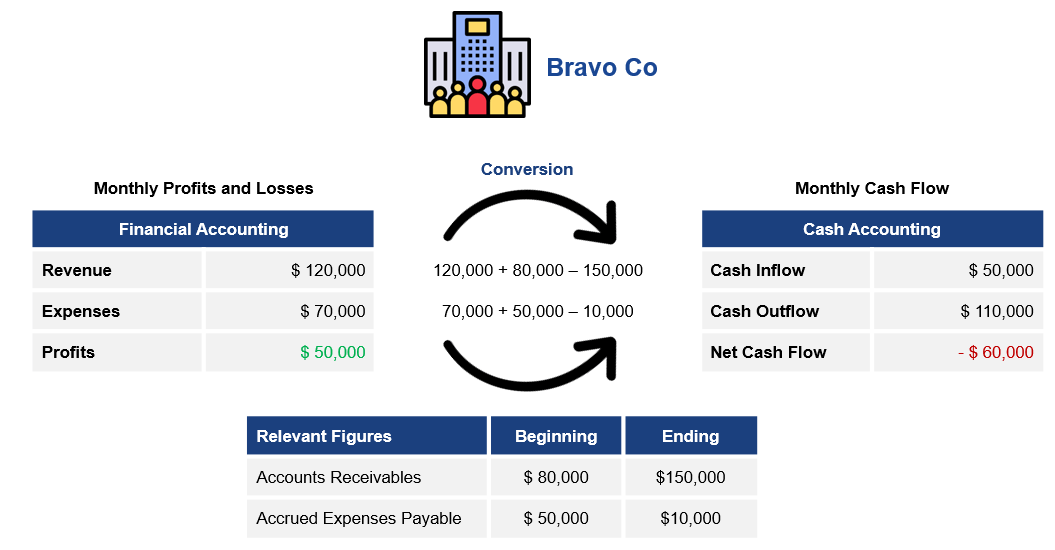

Illustrative example

To illustrate Cash Accounting, we could look at Bravo Co.

According to Financial Accounting standards, Bravo Co is profitable (S$ 50k profits).

Upon switching to Cash Accounting, the problem was apparent – Bravo Co paid their expenses upfront, and took a long time to collect their receivables, resulting in negative operating cash flow (S$ 60k loss).

You could apply the following formulas to switch from Financial Accounting to Cash Accounting:

- Cash inflow = Revenue + Beginning Accounts Receivables - Ending Accounts Receivables

- Cash outflow = Expenses + Beginning Accrued Expenses Payable - Ending Accrued Expenses Payable

Illustration of Financial Accounting versus Cash Accounting

What is cash flow bleed?

A negative cash flow is also known as “cash flow bleed”. While the definition of cash flow bleed defers between industries and companies, as a general rule of thumb, your company could be classified as undergoing financial distress if your company experiences negative operating cash flow for 2 consecutive years without signs of improvement.

Step 2: Diagnose the reasons for your bleed

Doctors must first diagnose their patients’ underlying disease before they can treat their symptoms. Similarly, it is important to first diagnose the reason for your company’s cash flow bleed before we develop any turnaround strategies.

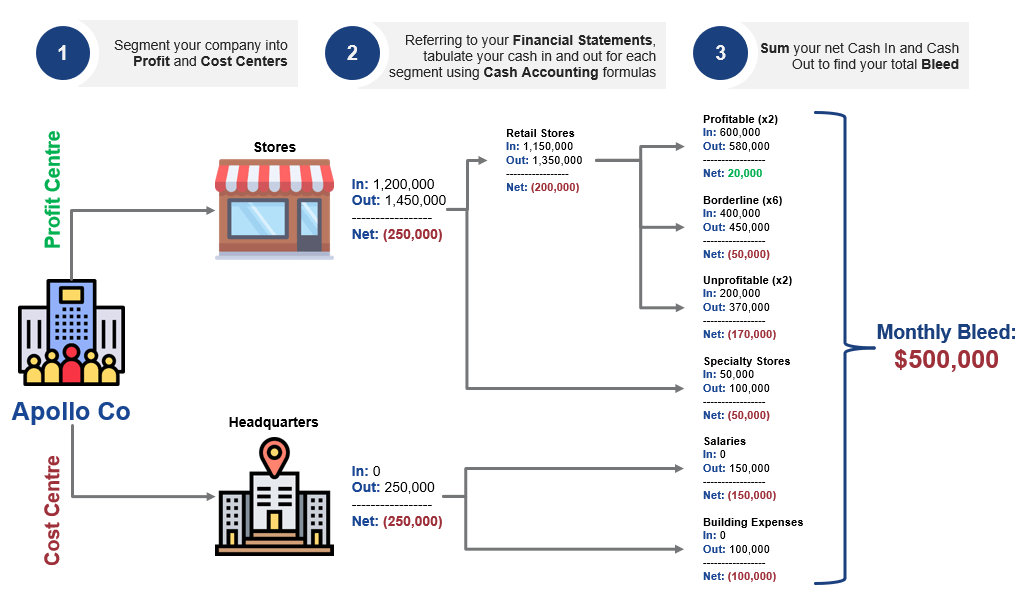

What are profit centres and cost centres?

To diagnose the reasons for the bleed, segment your company into profit and cost centres. Profit centres are responsible for revenue generation (as well as revenue-related costs), while cost centres only incur costs.

Examples of profit centres could include the individual revenue-making channels such as online sales channels, or the individual offline retail outlets. Examples of cost centres could include the following departments: accounting, customer service, human resources, among others. Note that these examples may or may not be relevant for your company, depending on your company’s industry and revenue model.

In general, there are two possible reasons for a company’s cash flow bleed:

- Your profit centres are profitable as a whole, but are not making enough to cover the outflow of your cost centres

- Your profit centres are loss-making as a whole, and together with the cost centres, they worsen your company’s overall net cash outflow

Illustrative example

Apollo Co is a retailer with a monthly bleed of S$500k.

To gain a better understanding of the reasons for Apollo Co’s bleed, we segmented their profit centres (each store outlet is 1 profit centre) and their cost centre (Apollo’s headquarters).

Looking at Apollo’s bleed, we can see that they fall under the second category – their profit centres (stores) are unprofitable as a whole (overall S$ 250k loss) and accounted for half of their total monthly bleed (S$ 500k loss). Note that while Apollo’s profit centres are unprofitable, there are some individual stores that are profitable.

Illustration of Bleed Diagnosis

Step 3: Estimate your company’s cash runway

A turnaround strategy typically takes time, and time is a luxury that distressed companies cannot afford. When your company is bleeding, you are burning through your cash reserves, loans, or other sources of cash. These cash resources are limited and will run out eventually.

The duration of how long your cash resources will last is known as the cash runway. More often than not, distressed companies are still in the midst of their turnaround strategy when they run out of cash and declare for bankruptcy. This could be avoided with proper estimation and management of your company’s cash runway.

You could apply the following formula to estimate the length of your runway (in months):

- Runway (Month(s)) = (Total Value of Cash or Cash Equivalent) / (Monthly Bleed)

As an example, we could look back at the Apollo Co case study. Apollo Co has a monthly bleed of S$ 500k. Suppose that Apollo Co has a cash reserve of S$ 1mn, their estimated runway would therefore be only 2 months (1mn / 500k = 2).

With an in-depth understanding of your cash flow situation, the next step would be to extend your runway to buy your company enough time for you to develop your turnaround strategy and get your company back to breakeven or profitability. This will be covered in Part 2 of our Turnaround Strategy Thought Leadership article, which will be uploaded in the near future.

3. We are here to help

If you are a business owner and you require assistance with any of the above steps, or if you have completed the above steps, but are wondering how to develop your turnaround strategy, feel free to reach out to us here to have a discussion.

Connect With Us!